Research ● 2024 ● 13 min read

Navigating financial legal problems in Victoria: Understanding help-seeking behaviour to enhance intervention

In this article

Print & save

Share

Navigating financial legal problems in Victoria: Understanding help-seeking behaviour to enhance early intervention

A research report by Justice Connect.

This report wouldn’t have been possible without the generous support of the Victoria Law Foundation.

Why we completed this research

There is more that services can do to address rising financial legal need through early intervention.

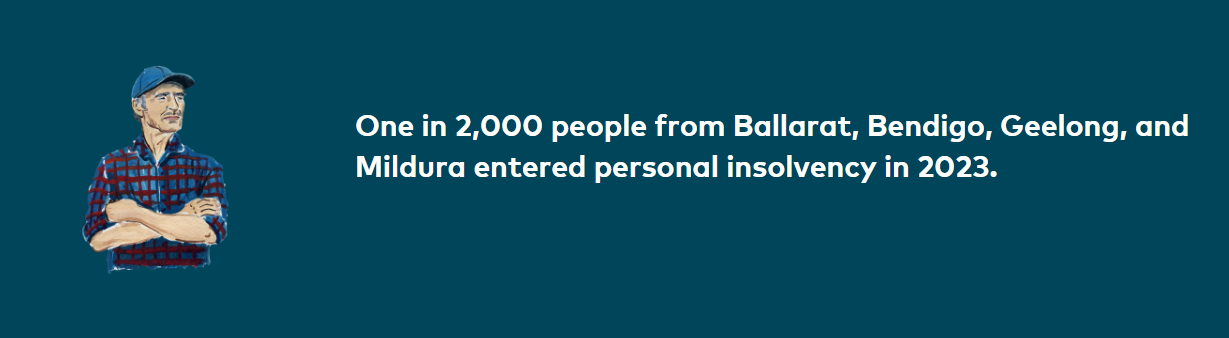

In Victoria, debt enforcement and personal insolvency have persisted as common; year by year, and amidst the cost-of-living crisis, we see financial legal problems and demand for legal and financial community services continue to increase. These figures do not capture the full extent of legal need related to financial legal problems, and it can be assumed that many more Victorians are currently experiencing a journey toward personal insolvency through debt enforcement.

For many, financial legal problems lead to an ongoing cycle of negative consequences, destabilising life for many years and sometimes permanently. Being made involuntarily bankrupt is often described by those that experience it as “the worst experience of their lives”.

Not only are serious financial legal problems common and destructive for those who experience them, they are also preventable. This research emerged from Justice Connect’s service provision to self represented litigants in the Victorian and Federal Courts. Our lawyers identified that by the time matters reached the courts they were often entrenched, more complex, and already impacting the wellbeing of debtors and their families. However, they also identified that the legal problems they were seeing could have been resolved at a much earlier stage.

Accordingly, Justice Connect’s research report “Navigating Financial Legal Problems” explores what happens to a person living in Victoria when they experience a financial legal problem, how debtors behave across each stage of their legal problem including at its onset, and what does not happen with respect to the timely intervention of community services. It identifies that there is more that services can do to address rising financial legal need.

The research and report centres on the experience of our research participants – people with lived experience of financial legal problems – and draws on a strength-based approach to making recommendations. We explore:

- Who is vulnerable to financial legal problems?

- How do debtors behave before, at the onset of, during, and after a financial legal problem?

- How does service availability, design, and delivery align with debtor behaviour?

- What opportunities are there to expand the provision of early intervention support for financial legal problems?

- Can we do more with the resources we currently have to better respond to financial legal need?

Explore the report:

Executive summary

Read time: 10 minutes

Full report

Read time: 1 hour and 40 minutes

Watch our webinar

To celebrate the launch of the research report, Justice Connect researchers held a webinar to explain key insights from our research, and its implications on the financial legal services sector.

By watching this webinar recording you can learn more about how people in Victoria navigate financial legal problems and what our findings mean for the free legal and financial sectors.

What we looked at

People with lived experience are at the centre of this report. The study of their behaviour ensures that they are at the centre of service design, evaluation, and provision across our sector.

This comprehensive, human-centred report outlines the context, rationale, methodology and findings of an 18-month long research project completed by researchers embedded in Justice Connect’s Access Program.

About the importance of learning from lived experience, participant Maryam* told us:

“I wish I lived my life responsible for the outcome of my family situation. I wish I had gotten help before I got married. But you know what? All my kids know what to do now, they all have insurance, they know not to get credit cards. You live, you learn, and you help your family. And I have a job now. This experience helped me build up the courage to go and get a job for the first time in my life. I was 50 years old when I stepped out of my home for the first time, and if this all hadn’t happened, neither would that.”

Key findings

Legal capability must be at the core of how we design, evaluate, and deliver services.

The following findings were identified using a strength-based approach to researching financial legal problems, debtor behaviour, and early intervention. A strength-based approach utilises co-design methods to focus on the resources, skills, and strengths that consumers currently possess, leveraging their agency to develop future solutions.

For financial legal problems, this requires working out what Victorian debtors currently do when faced with unmanageable debts, the resources they already have at their disposal, and the pathways they prefer or are inclined to use when searching for help. By understanding these factors, the problem we’re addressing can be reframed and our strategies tailored accordingly.

The problem identified in this research, therefore, lies in the way that services are currently designed and the aspects of service delivery that do not meet the express and latent financial legal need in the Victorian community early enough.

Part one provides a rationale for the focus on certain priority groups and the types of legal problems and online self-help resources explored. It introduces the participants and describes the methods and resources used to better understand the journeys of people in the ‘missing majority’.

Any person, provided they experience a certain combination of financial strain, life events, non-financial vulnerability, or mistreatment regarding a loan or the law, can go bankrupt.

All participants experienced some kind of debt enforcement. An overwhelming majority of them held unregulated or unsecured debts. Unregulated and unsecured debts are commonly held across Victoria, and people with smaller debts are very vulnerable to debt enforcement – this leaves us with a very large group of Victorians in the “at-risk” group.

(Figure 1)

There are some cohorts of people that are more vulnerable to debt enforcement than others.

92% of participants identified as having experienced one or more “life event” associated with vulnerability prior to, or at the onset of, their financial legal problem. For most, this had a direct impact on whether they could manage their debt obligations.

(Figure 2)

Financial legal problems are also socially patterned.

There is a moderate correlation between the distribution of poverty and personal insolvency. This means in regions experiencing greater rates of financial disadvantage, we might expect to see greater rates of personal insolvency. This correlation increases for women and for people over 65 years of age.

“Life events” tend to occur before a financial legal problem emerges or right at the start, which means they offer an opportunity for prevention or early intervention.

Debtors look for help when they experience a “life event”, and sometimes look for help for the impact that life event has on their financial situation. Sometimes, but not most of the time, accessing general help leads to help from a financial counsellor or lawyer.

(Figure 3.1)

(Figure 3.2)

Whether or not general help-seeking leads to appropriate help for a person’s financial legal problem, depends on the health of the referral relationships in the relevant sector.

Where our participants experienced family violence or coercive control, a serious or sudden illness, housing insecurity, or mental ill-health, they were generally referred to a legal service that could help with their financial legal problem.

Other experiences are less likely to lead to a referral for early intervention, as certain groups vulnerable to personal insolvency cannot access services prior to their legal problem becoming critical. This is due to the operation of asset tests and the assumption that individuals with business experience have sufficiently high legal capability to self-help, both of which are pervasive across the free legal sector.

“There is a massive service gap for people who are asset rich but income poor. For example, older people who have paid off their mortgage but live on the pension.” Service Provider Participant

For debtors who experience the loss of their job, or main source of income, this cohort’s dependence on their owned family home for stability makes them particularly vulnerable in the event of bankruptcy, given the likelihood that they will lose it.

There remains a significant proportion of Victorians – those with compounding vulnerabilities and those without – who are not connected with legal or financial assistance in a timely manner.

Debtors exhibit a strongly held motivation to resolve their legal problem at its onset, defined as the moment they first realise they are unable to meet their debt obligations: 96% of participants looked for help from a professional, their creditor, or someone in their personal networks when their legal problem began.

Most participants look outside of their personal networks, seeking help from either a professional or their creditor. Lawyers were the most sought-after professional, with 63% of our participants thinking about looking for one and 50% making an initial enquiry.

(Figure 4)

Despite proactively searching for help, participants weren’t sure that there would be help available to them. They nonetheless recognised a need for expertise.

70% of participants used the internet to look for help, 61% spoke to an organisations or person over the phone, and 39% looked in person. All interviewed participants that reported help-seeking over the phone or in -person used the internet to narrow down services and find their contact information.

“So much of the legal response to financial issues relies on crisis” Service Provider Participant

“I love google because it doesn’t judge you for the way you ask it for help.” Interviewed Participant

No participants reported getting help for their problem early, and most of them looked for it.

Help-seeking motivation diminishes over time. This means that the longer financial legal problems go on, the less likely they are to continue to search for it.

(Figure 5)

(Figure 6)

(Figure 7)

Despite this, as time went on, participants were becoming increasingly aware that their journeys were headed toward a legal cliff-edge, reporting increased understanding of the seriousness and consequences of inaction.

(Figure 8)

(Figure 9)

(Figure 10)

“Services string you along. They keep saying I’ll call you back, and then they don’t, or they say sorry never mind, we can’t help you”. Interviewed Participant

“You contact one person and they so go to this person, and then that person says go to that person. You don’t ever get any service. You get overwhelmed… it is like a revolving door.” Interviewed Participant

To find help, debtors must be resilient, and hold certain, necessary legal capabilities. They must find a service on their own, with incomplete, unclear, or overly complicated information at their disposal. They are forced to cast a wide net when applying for services, even though they don’t want to. Then, when they are declined a service by one provider, they must promptly look for another on their own or be able to follow cold referral instructions. They must also be willing to receive a service that is different to what they anticipated, and less intensive than they want or might require.

“Most services only provide discrete help for debt matters.” Service Provider Participant

This research has identified that referral roundabouts continue to affect help-seeking, discouraging and interfering with the timely provision of financial legal help. When a debtor enters the referral roundabout, time doesn’t stop. Their legal problem continues to get worse, the size of their underlying debt grows, and they start facing threats of court. Many participants report failing to access help until after a judgement is awarded against them.

There are many reasons why referral roundabouts are pervasive, and most of them relate to how insufficiently human-centred the application, assessment, and offboarding processes are at legal services.

The full report explores these reasons and offers solutions, in the form of recommendations.

“Getting help is harder for bankruptcy than other things. Its really difficult, you get into a fog, you feel as though your life is pretty well turned upside down and you can’t think straight. But you’re looking, you’re desperately looking for help.” Interviewed Participant.

This research has identified the legal capabilities that a debtor must have to effectively navigate the current service ecosystem for financial legal problems.

- Legal knowledge is required to understand that difficulty meeting debt obligations is a problem that lawyers or other professionals can help with. Its also essential to interpreting eligibility guidelines when looking for an appropriate service.

- Digital literacy means that debtors can use the internet to their advantage, finding relevant services to apply to quickly.

- Proactivity means looking for help quickly, before financial legal problems escalate. This is necessary given response and wait times at legal services.

- Motivation and Resilience is important, as most debtors must navigate the system alone. This includes making applications, following cold referral instructions, and dealing with frustration.

- Responsiveness is necessitated by services, who require debtors to perform tasks throughout service delivery, including gathering documents, filling in forms, answering emails, and making calls.

- Legal skills are important as most financial legal services are discrete. After getting some advice, most debtors need to perform legal tasks on their own.

- Reciprocity benefits the legal help ecosystem, as most service evaluations (and therefore service improvements) rely on feedback provided by clients at the end of a service.

However, as reiterated by the findings of this research, human behaviour, legal capabilities, and legal needs are diverse and cannot be appropriately mirrored by the common one-size-fits-all approach to service design. This emphasises the importance of designing financial legal services to meet the needs of debtors at all capability levels.

Navigating the ecosystem of free legal help, while a crucial first step, is not the only threshold requirement to problem resolution; we cannot expect that a debtor’s legal problems are resolved by virtue of them coming in our services’ front door.

Not only are legal capabilities diverse across the Victorian population, but they are subject to change across the life of a debtor’s legal problem, particularly in periods of high stress. Participants with commercial experience or who had accessed the courts before, might have begun their help-seeking journey with high legal capabilities. But, by the time their legal problem is advanced, high stress impacts their ability to continue to self-advocate.

“I know from my experience that it took a long time to get the spectrum of advice I needed. By the time [a service] would help me, I was at court.”

Resolving financial legal problems through service provision, therefore, requires regular re-assessment of a client’s legal capabilities and a dynamic approach to service provision that can scale up and scale down as necessary.

“Some people require wrap-around and multidisciplinary assistance to resolve their problem without retraumatising them.” Service Provider Participant

“Often you don’t even realise you have do to something [after receiving a service].” Interviewed Participant

As economic and regulatory conditions shift, so does the behaviour of creditors. The research identifies that the overall decrease in volume of involuntary bankruptcies since 2019 does not equate to a change in creditor behaviour away from debt enforcement. Rather, it reflects a change in creditor strategy.

As creditors are increasingly viewing involuntary bankruptcy as an ineffective and expensive tool to recoup owed monies, the enforcement of lower court judgement debts is emerging as a central tool of creditor aggression. These tactics generate similar outcomes to involuntary bankruptcy in material terms for debtors, garnishing debtor’s take home wages, selling debtor’s property, and driving social isolation with consequences for wellbeing.

They also represent accelerated processes of debt enforcement with fewer protections (or fewer opportunities for intervention) for debtors. As enforcement trends earlier, crisis driven service provision which considers bankruptcy as the key intervention opportunity, may no longer be servicing a significant cohort of Victorians with financial legal problems.

The trend away from personal insolvency as a debt enforcement measure is not a fall in overall debt enforcement but rather a redirection.

More latest news

Donate now

Together, we can make access to justice a reality for everyone. Act now to give people who are struggling a brighter future.